By Region - By Hotel Category - By Ownership Model - By City

City Spotlights: Barcelona - Madrid - Andalusia

Spain's hotel sector closed 2025 with full-year ADR of EUR 166.1 a 4.8% increase that was four times the European average of 1.2% RevPAR growth of 5.5% against Europe's 1.5%, national occupancy of 75.5%, independent hotels holding 57.65% of Spain's hospitality market share, and a EUR 430 million sale of Mare Nostrum Resort and a EUR 175 million acquisition of Fairmont La Hacienda demonstrating sustained institutional investor confidence in Spain's boutique-adjacent leisure hospitality assets.

MARKET SYNOPSIS

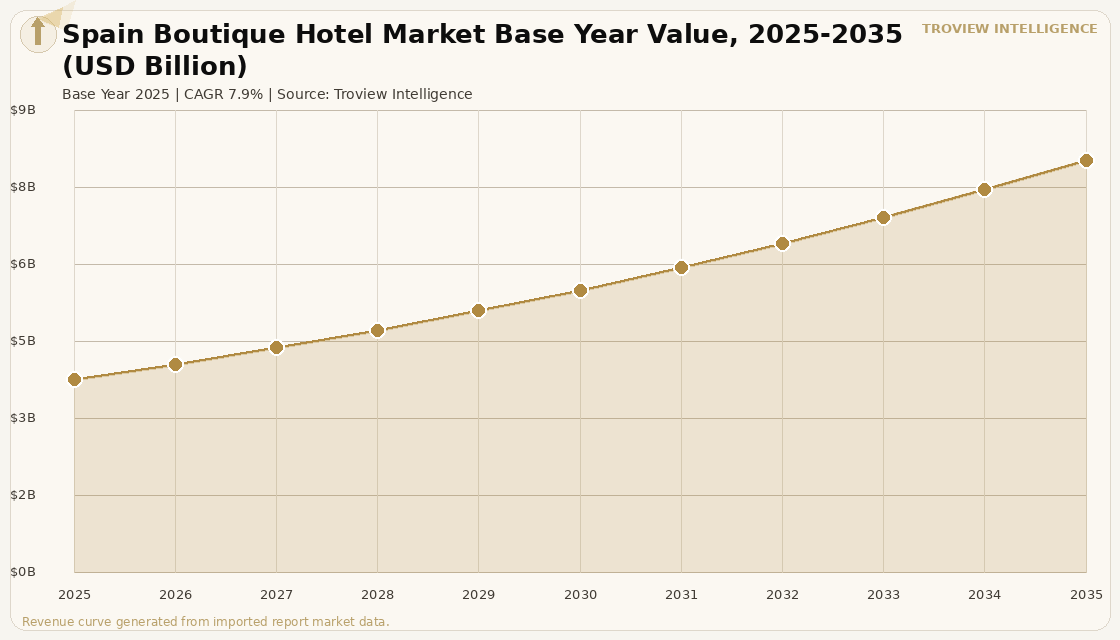

The Spain boutique hotel market size was USD 3.84 Billion in 2025 and is expected to register a revenue CAGR of 7.9% during the forecast period, reaching USD 8.19 Billion by 2035. Spain is Europe's strongest-performing major hotel market, with the country's hotel sector closing 2025 with full-year ADR of EUR 166.1 growing 4.8% year-on-year, four times Europe's 1.2% average and RevPAR growth of 5.5%, more than three times Europe's 1.5% average, per STR and Cushman and Wakefield Hotel Barometer data published March 2026. Independent hotels hold 57.65% of Spain's hospitality market share by revenue per verified hospitality market data, reflecting the country's deep independent boutique operator tradition that spans urban design hotels in Barcelona and Madrid, wine-country paradors in La Rioja and Ribera del Duero, and coastal boutique resorts across Andalusia and the Balearic Islands. Spain ranked among the world's top three tourist destinations globally, with sustained demand from Northern European leisure source markets the United Kingdom, Germany, France, and the Netherlands providing a structural occupancy floor for boutique hotel operators across all seasons in Mediterranean coastal and urban markets. For instance, in 2025, the EUR 430 million sale of Mare Nostrum Resort in Tenerife and the EUR 175 million acquisition of Fairmont La Hacienda by institutional investors confirmed that Spain's premium leisure hotel segment of which boutique-positioned properties are the most illiquid and highest-ADR component attracted the largest single-asset transactions in Spanish hotel investment history, per Christie and Co Business Outlook 2026 Spain reporting. These are some of the key factors driving revenue growth of the market.

Spain's boutique hotel investment market in 2025 was dominated by national buyers who accounted for 69.5% of total hotel investment transactions, with Spanish operators and private real estate investors purchasing the majority of boutique hotel assets as foreign institutional capital directed its Spain hospitality allocation toward larger-format resort transactions. Barcelona's hotel sector posted H1 2025 ADR of EUR 195.5 Spain's second-highest city ADR behind Marbella at EUR 315 with supply constrained to only 0.1% year-on-year growth due to the city government's ongoing hotel licence moratorium, creating ADR growth conditions where boutique hotels with existing licences enjoy a structural pricing advantage over any competitive new supply. The Christie and Co 2026 Business Outlook confirmed that resort markets dominated transaction activity, with Tenerife emerging as a key hotspot, and that Madrid's hotel pipeline of approximately 2,300 rooms tilts toward boutique independents, confirming that boutique hotel development is the dominant format for new hotel supply creation in Spain's urban gateway markets where large-format chain development is constrained by land availability and planning restrictions.

However, the Spain boutique hotel market faces structural constraints that moderate sustainable growth. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that Spain as a country dependent on natural gas imports for electricity generation in the non-solar portions of its energy mix must absorb through higher utility costs for boutique hotel operators who cannot access group energy procurement contracts at the scale available to large hotel chains. Overtourism management policies in Barcelona including proposed doubling of the city tax, restrictions on tourist apartment licences, and proposals to reduce cruise ship terminal capacity from seven to five are creating a complex regulatory environment for boutique hotel operators that simultaneously benefits existing licensed properties through ADR uplift and creates political risk for the tourism-dependent business model from local resident anti-tourism sentiment that has generated public protests and vandalism incidents against tourist infrastructure. The competitive entry of well-capitalised soft-brand collections including Marriott Autograph Collection, Hilton Curio Collection, and Ennismore's 25hours Hotels into Spanish gateway cities is providing chain-affiliated boutique alternatives that erode the market share of truly independent boutique operators who cannot match the distribution infrastructure of 200-million-member loyalty programmes. These factors substantially limit Spain boutique hotel market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Spain's boutique hotel market in 2025 is one of the most instructive case studies in European hospitality investment. The country achieved 4.8% ADR growth against a European average of 1.2% and it did so not by adding supply, but by restricting it. Barcelona's hotel licence moratorium has been in place since 2015. The properties that already have licences in the Eixample, the Gothic Quarter, and Born have enjoyed a decade of compounding ADR growth that no operational improvement could have generated without the supply cap. That is not a coincidence. It is a policy-engineered scarcity premium. The boutique hotel investor who holds a licensed property in central Barcelona today owns what is effectively a perpetual ADR premium machine as long as the moratorium continues. The risk is not operational. The risk is the political pressure from residents who want the moratorium extended to cover other formats, other districts, and potentially other tools that could affect the visitor economics of the hospitality market more broadly." Troview Intelligence Head of Spain Boutique Hotel Market Research

SEGMENT INSIGHTS

Three Cities Shaping Spain's Boutique Hotel Market

| H1 2025 ADR | H1 2025 RevPAR | Supply Growth (YoY) | Hotel Licence Status |

| EUR 195.5 (+3.1% YoY) | EUR 149.80 (+1.6% YoY) | 0.1% virtually zero | Moratorium since 2015 in central districts |

Barcelona is Spain's highest-ADR major hotel market and one of Europe's most supply-constrained boutique investment destinations, with H1 2025 ADR of EUR 195.5 Spain's second-highest city rate and above the national ADR of EUR 166.1 supported by hotel supply that grew only 0.1% year-on-year in the year to May 2025 per Hospitality Net Barcelona Hotel Market Spotlight reporting. The city government's hotel licence moratorium in central districts, in effect since 2015, has created a decade-long compounding ADR advantage for existing licensed boutique hotel operators in Eixample, Gothic Quarter, Born, and Barceloneta the districts with the highest international tourist footfall while making hotel licences themselves the primary value driver in boutique hotel transactions where the asset's operational revenue is secondary to the scarcity premium embedded in the licence. Barcelona's H1 2025 GOP margin reached 45.1% up from 43.9% in H1 2024 with GOP flow through of 66.9%, confirming that the supply-constrained ADR growth is delivering operational leverage with revenue growth outpacing cost growth at the property level per Hospitality Net data. Investment in Barcelona's hotel sector reached EUR 518 million, with institutional investors accounting for 63% of total investment volume, confirming sustained professional capital deployment into a market where boutique hotel licences are among Europe's most valuable hospitality real estate assets.

| H1 2025 ADR | H1 2025 RevPAR | ADR Growth H1 2025 | Hotel Pipeline Profile |

| EUR 179.6 (+6.6% YoY) | EUR 137.4 (+6.7% YoY) | Highest of Spain's major cities | ~2,300 rooms boutique-tilted |

Madrid recorded the fastest ADR growth of any major Spanish city in H1 2025, with ADR of EUR 179.6 representing a 6.6% year-on-year increase and RevPAR of EUR 137.4 growing 6.7%, outperforming Barcelona's 3.1% ADR growth and 1.6% RevPAR growth during the same period per Cushman and Wakefield Spain H1 2025 hospitality performance data. Madrid's hotel pipeline of approximately 2,300 rooms tilts toward boutique independents , confirming that new boutique hotel product is the dominant format for capacity addition in the Spanish capital where large-format chain development is constrained by the historic city centre's UNESCO protection zones and land availability. Conference-driven weekday corporate demand in Madrid accelerates recovery of corporate ADR beyond 2019 benchmarks, providing boutique hotels in Salamanca, Chueca, and Malasana with a dual revenue stream combining weekend leisure tourism from European city-break travellers with weekday MICE demand from Spain's growing business conference calendar.

| Marbella ADR 2025 | Key 2025 Transaction | Occupancy Range | Market Profile |

| EUR 315 (Spain's highest city ADR) | EUR 175M Fairmont La Hacienda acq. | 67.2% (profitability over volume) | Luxury boutique, resort, private villa |

Andalusia is Spain's highest-ADR boutique hotel market by destination, with Marbella achieving full-year 2025 ADR of EUR 315 Spain's highest of any tracked city or destination, more than 1.9 times the national ADR of EUR 166.1 while maintaining occupancy of 67.2% that demonstrates a deliberate profitability-over-volume strategy favoured by Marbella's luxury boutique and resort operators who maximise ADR at moderate occupancy rather than competing on rate to achieve high fill rates. The EUR 175 million acquisition of Fairmont La Hacienda in Andalusia and the EUR 430 million sale of Mare Nostrum Resort in Tenerife in 2025 confirmed that institutional capital is targeting Spain's premium leisure boutique segment through large-format transactions, with Fairmont La Hacienda representing a branded boutique resort investment that combines Accor's Fairmont brand infrastructure with the ADR premium of Marbella's established luxury leisure destination identity. Andalusia's broader boutique hotel market spanning Seville's historic centre, Granada's Albaicin neighbourhood, and the white villages of Ronda benefits from year-round cultural tourism demand from European heritage travellers that provides occupancy floors independent of the coastal resort seasonality affecting Marbella and Costa del Sol beach properties.