By Zone - By Facility Type - By Specialisation - By Payer

Zones: CBD and Inner City - Northern Suburbs - Western Sydney - South and Sutherland - Hills District

Sydney is Australia's largest outpatient and ambulatory care facility market, hosting Royal Prince Alfred Hospital and St Vincent's Hospital as primary specialist outpatient anchors, Ramsay Health Care and Healthscope as the dominant private ambulatory operators across western and northern suburbs, NSW Health invested AUD 120 million in Blacktown and Mount Druitt Hospital upgrades including 60 additional beds in May 2025, ambulatory surgery accounts for over 90% of Sydney cataract procedures and 75% of hernia repairs, and Ramsay Health Hub digital front door now at 39 Australian sites is transforming outpatient pre-procedure administration across the private ambulatory network.

MARKET SYNOPSIS

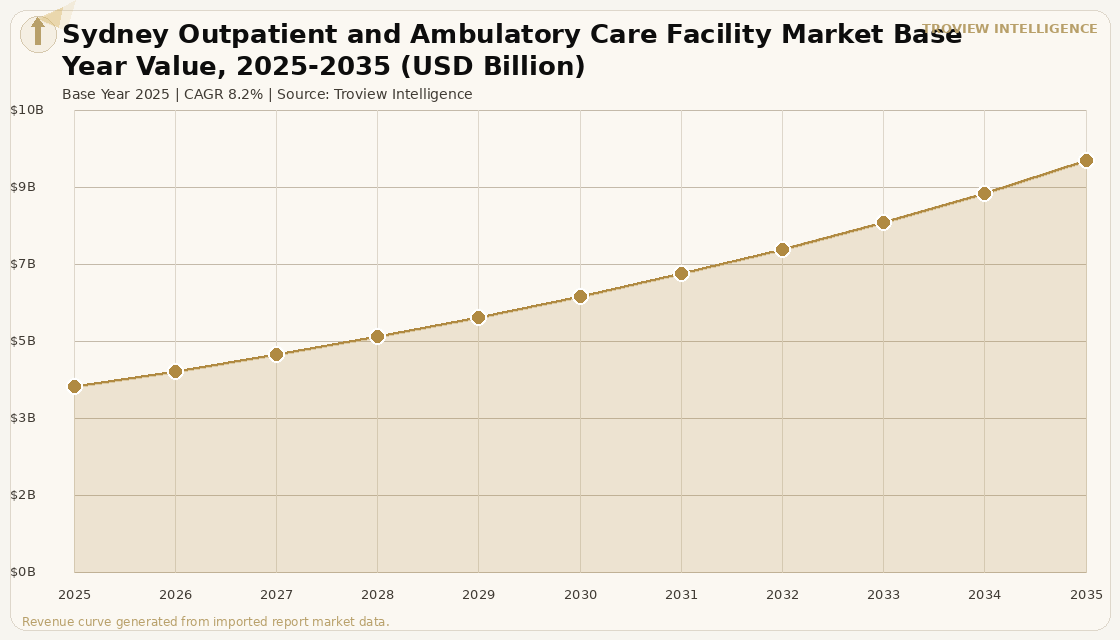

The Sydney outpatient and ambulatory care facility market size was USD 4.18 Billion in 2025 and is expected to register a revenue CAGR of 8.2% during the forecast period, reaching USD 9.24 Billion by 2035. Sydney is Australia's largest and most complex outpatient and ambulatory care market, serving a metropolitan population of approximately 5.3 million through an integrated network of public hospital outpatient departments, private day-surgery centres, specialist clinics, diagnostic imaging services, and community health centres across the Sydney Basin's geographically diverse catchment areas. The Sydney Local Health District hosts Royal Prince Alfred Hospital one of Australia's highest-volume specialist outpatient referral centres alongside Concord Repatriation General Hospital, Canterbury Hospital, and a network of community health and ambulatory care facilities that collectively manage tens of millions of non-admitted patient care events per year within the LHD boundaries. NSW Health's broader Sydney metropolitan district network spanning twelve Local Health Districts from South Western Sydney to Northern Sydney operates the largest public hospital outpatient network in Australia by population served. For instance, in May 2025, the Australian Government announced a AUD 120 million investment to upgrade Blacktown and Mount Druitt Hospitals in Western Sydney, adding 60 additional beds across the two facilities and expanding ambulatory and outpatient care capacity in a catchment of approximately 440,000 residents that has experienced sustained population growth and corresponding demand for accessible outpatient services, per verified Australian healthcare market data. These are some of the key factors driving revenue growth of the market.

Sydney's private outpatient and ambulatory care sector is led by Ramsay Health Care and Healthscope now increasingly under Ramsay's expanding network following the ACCC's February 2026 approval of Ramsay's acquisition of National Capital from Healthscope which collectively operate the majority of private hospital day-surgery capacity across Sydney's inner, northern, western, and southern suburban markets. Sydney is the primary geographic market for Ramsay Health Care's Australian operations, which benefited from solid activity growth and improved private health insurance indexation in FY25, with the company investing in digital front door transformation through Ramsay Health Hub at 39 Australian sites, digital medical records, and outpatient telehealth for mental health that are progressively reducing administrative friction for ambulatory patients navigating pre-procedure and post-procedure outpatient interactions. Sonic Healthcare headquartered in Sydney operates the largest private pathology and diagnostic imaging network in Australia, with Sydney as the primary market for its ambulatory diagnostic service volumes that support the outpatient diagnostic ordering of thousands of specialist and GP clinicians across the city.

However, the Sydney outpatient and ambulatory care facility market faces structural constraints that limit the pace of capacity expansion. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating medical consumable supply chain cost pressures and energy cost inflation that affect Sydney ambulatory facilities whose operating cost base includes significant consumable spend on disposable surgical supplies, diagnostic reagents, and pharmaceutical agents that are subject to global freight and energy cost pass-through. Sydney's healthcare workforce shortfall concentrated in specialist nursing, anaesthetic nursing, surgical technicians, and allied health professionals limits throughput at capital-sufficient ambulatory surgical centres and day-surgery facilities that are physically capable of serving higher patient volumes but cannot staff additional operating lists due to workforce supply constraints. The structural gap between public hospital outpatient waiting lists where elective outpatient specialist consultation waiting times can exceed 12 months across Sydney's busiest Local Health Districts and the capacity of the private ambulatory sector to absorb redirected demand is creating access equity issues for patients without private health insurance who cannot access timely outpatient specialist care through the public system. These factors substantially limit Sydney outpatient and ambulatory care facility market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Sydney's ambulatory care market has a geographic dimension that other Australian cities do not face at the same scale. The city is fragmented across twelve Local Health Districts covering a geographic footprint that stretches from Penrith in the west to Manly in the north to Sutherland in the south. The infrastructure that serves CBD and inner-city residents Royal Prince Alfred, St Vincent's, Sydney Private Hospital has little relevance to the accessibility needs of a patient in Blacktown or Campbelltown whose nearest public specialist outpatient clinic has a 12-month wait. The AUD 120 million Blacktown-Mount Druitt upgrade addresses the acute end of this problem. The ambulatory care market opportunity for private investors is in the western and south-western Sydney corridor fastest population growth, lowest current private hospital density, highest unmet specialist outpatient demand where a well-capitalised day-surgery centre with a strong specialist referral network can generate sustainable procedure volumes from a catchment that the public system cannot serve within clinically reasonable timeframes. Ramsay understands this. Their western Sydney network exists precisely because the geography creates captive demand for private ambulatory alternatives to public hospital wait times." Troview Intelligence Senior Analyst, Sydney Healthcare Facility Markets

SEGMENT INSIGHTS

Zone Deep-Dives

CBD and Inner City ROYAL PRINCE ALFRED, ST VINCENT'S, SPECIALIST SUITE CONCENTRATION

| Anchor Institutions | Specialist Suite Hubs | Key Operators | Zone Character |

| Royal Prince Alfred, St Vincent's | Macquarie St, Edgecliff, Surry Hills | Ramsay, Healthscope, Sydney Private | Tertiary referral, high-complexity outpatient |

The CBD and inner-city zone is Sydney's primary specialist outpatient hub, anchored by Royal Prince Alfred Hospital which operates one of Australia's largest specialist outpatient clinic networks spanning more than 80 outpatient clinic types across medicine, surgery, oncology, and allied health and St Vincent's Hospital in Darlinghurst, which provides specialist outpatient services in cardiology, HIV medicine, psychiatry, and liver disease through a major ambulatory care and outpatient clinic complex. Macquarie Street in the CBD hosts the highest concentration of specialist medical consulting suites in Australia, with cardiologists, ophthalmologists, gastroenterologists, orthopaedic surgeons, and other specialists operating private consulting rooms that serve both private patients and public hospital outpatient referrals within the same building environments. Sydney Private Hospital in Surry Hills and Prince of Wales Private Hospital in Randwick are the primary inner-city private ambulatory surgical centres, offering same-day surgery across ophthalmology, gastroenterology, orthopaedics, and general surgery for the inner-city and eastern suburbs private health insurance population.

| Primary Anchor | New Development | Zone Population | Key Private Operators |

| Macquarie University Hospital | Northern Beaches Hospital (opened 2019) | ~950,000 northern Sydney residents | Ramsay (Northern Beaches), Healthscope |

Sydney's northern suburbs zone hosts the Macquarie Park health precinct anchored by Macquarie University Hospital which operates as both a clinical facility and a clinical education site for Macquarie University's medical school with an expanding specialist outpatient clinic network serving the rapidly growing population of north-western Sydney including Ryde, Lane Cove, and Macquarie Park's residential developments. The Northern Beaches Hospital, opened in 2019 as Australia's first fully integrated public-private hospital, operates under a public-private partnership with Healthscope managing the private component, providing day-surgery, specialist outpatient, and emergency services to the Northern Beaches Local Health District's population of approximately 280,000. The northern suburbs zone benefits from high private health insurance penetration with northern Sydney demographics characterised by above-average income and above-average private health insurance take-up that supports strong private ambulatory procedure volumes and specialist consultation activity across the zone's day-surgery centres and specialist suite buildings.

| Zone Population | NSW Health Investment | Population Growth Rate | Private Ambulatory Gap |

| ~2.0 million largest Sydney zone | AUD 120M Blacktown-Mount Druitt upgrade | Fastest in Sydney Metro | Lowest private day-surgery density in metro |

Western Sydney is the fastest-growing outpatient and ambulatory care facility zone in Sydney, serving a population of approximately 2.0 million across Parramatta, Blacktown, Penrith, Fairfield, and Liverpool local government areas that represents the city's largest geographic catchment and its most rapidly expanding population base driven by greenfield residential development and migration settlement patterns. The AUD 120 million NSW Government investment announced in May 2025 to upgrade Blacktown and Mount Druitt Hospitals adding 60 additional beds and expanding outpatient and ambulatory care capacity reflects the structural imbalance between western Sydney's population size and its public hospital outpatient capacity, where elective outpatient waiting times are among the longest in the Sydney metropolitan area for specialties including orthopaedics, gynaecology, and ophthalmology. Western Sydney has the lowest private day-surgery centre density of any major Sydney zone relative to its population, representing a structural investment opportunity for ambulatory surgical centre development targeting the growing private health insurance-holding population in the Parramatta, Norwest, and Blacktown catchments where Ramsay Health Care and competing operators have identified new facility development potential.