By Emirate - By Brand Tier - By Asset Type - By Source Market

Emirate Spotlights: Dubai - Abu Dhabi - Ras Al Khaimah

UAE RevPAR and ADR grew 11.9% year-on-year in the year to August 2025 per Knight Frank's UAE Hospitality Market Review, with Abu Dhabi recording RevPAR growth of 24% and ADR growth of 20.2%, Dubai posting RevPAR growth of 10.1% and an average luxury segment ADR of approximately AED 1,470 (USD 400), Dubai welcomed 19.6 million international tourists in full-year 2025 with hotel occupancy averaging 78.5%, and Atlantis The Royal's USD 1.4 billion development investment established the UAE as the global benchmark for ultra-luxury hotel development returns.

MARKET SYNOPSIS

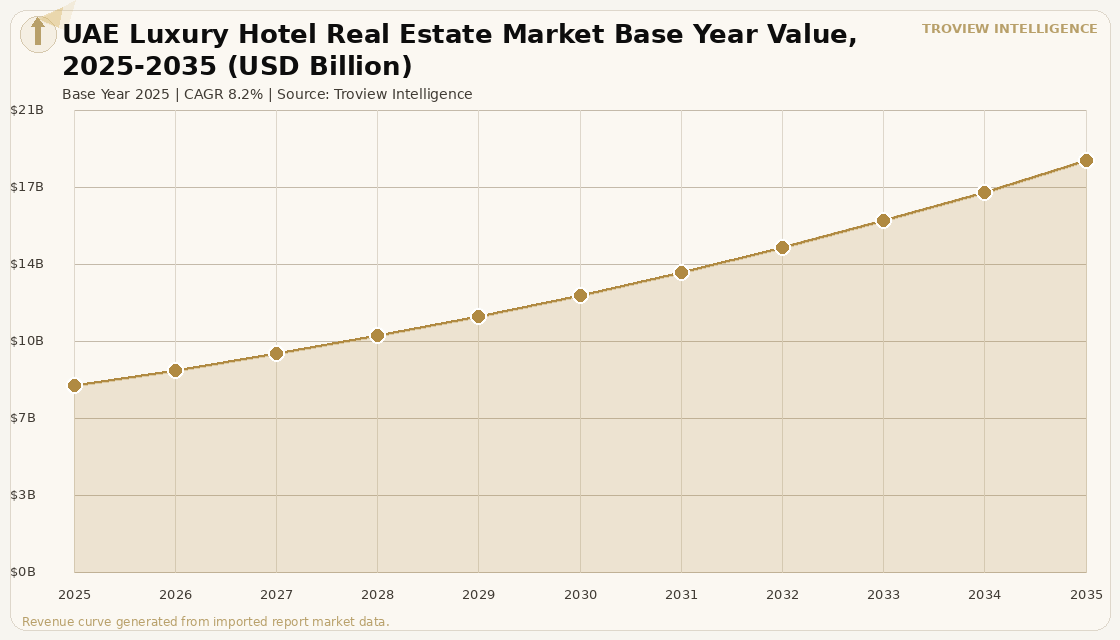

The UAE luxury hotel real estate market size was USD 8.46 Billion in 2025 and is expected to register a revenue CAGR of 8.2% during the forecast period, reaching USD 18.62 Billion by 2035. The UAE is the Middle East's dominant luxury hotel real estate market and one of the fastest-growing globally, with RevPAR and ADR growing 11.9% year-on-year in the year to August 2025 per Knight Frank's UAE Hospitality Market Review published October 2025, average occupancy across the UAE reaching 78.5% up 4% year-on-year and Dubai alone hosting 165,339 existing and upcoming hotel keys that represent 55.9% of the UAE's total upcoming supply. The UAE luxury hotel real estate market serves year-round HNWI demand from Western European source markets (21% of Dubai international visitors), South Asian visitors (15%), CIS and Eastern European visitors (14%), and MENA regional visitors (11%) per verified Department of Economy and Tourism data, providing a geographic demand diversification that insulates the market from single-source-market demand shocks. For instance, in 2024, the USD 1.4 billion Atlantis The Royal development opened on Dubai's Palm Jumeirah, completing a project at approximately USD 2.3 million per key across 795 rooms and suites that immediately generated luxury destination-level demand at ADRs exceeding AED 5,000 (USD 1,360) for suites during peak periods, confirming Dubai's ability to sustain ultra-luxury hotel development economics that cannot be replicated in any other Middle Eastern market at the same scale. These are some of the key factors driving revenue growth of the market.

The UAE luxury hotel real estate market is characterised by an increasingly mature investment landscape as Knight Frank's Autumn 2025 review confirmed, with an increasing range of regional and international investors attracted to a market characterised by strong growth fundamentals and a deepening pool of institutional capital. Dubai's luxury hotel segment specifically delivers average ADRs of approximately AED 1,470 (USD 400) and RevPAR of approximately AED 1,100 (USD 300), with the best-run luxury properties generating gross operating profit margins of 35 to 40% and providing equity investors with unlevered internal rates of return of 8 to 12% over a decade under steady-state conditions per verified hospitality investment analysis. Abu Dhabi recorded the strongest emirate-level performance in the year to August 2025, with RevPAR growing 24% and ADR increasing 20.2% year-on-year, driven by major international events, a 47% increase in cultural visitation, and a surge in MICE demand from government conferences per Abu Dhabi National Hotels investor disclosure. Ras Al Khaimah is emerging as the UAE's third luxury hotel investment market, with the planned Wynn Resort representing the region's first integrated entertainment resort targeting HNWI visitors who seek luxury experiences combining casino gaming with the UAE's established luxury hospitality infrastructure.

However, the UAE luxury hotel real estate market faces structural constraints that limit sustainable RevPAR growth over the forecast period. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are creating regional geopolitical uncertainty that, while not directly affecting UAE tourism infrastructure, represents a travel sentiment risk for Western European and North American HNWI source markets that collectively account for more than a third of Dubai's international visitor inflows. The delivery of 12,000 new luxury keys in Dubai by 2030 represents a structural supply risk: at current ADR levels and occupancy rates, the market can absorb incremental supply, but a simultaneous delivery of multiple large ultra-luxury assets during 2027 to 2029 could create a temporary RevPAR compression cycle before demand absorbs the new inventory. Staff cost pressures with personnel costs constituting 35 to 40% of hotel operating expenses in Dubai, amplified by expatriate workforce requirements including housing and transportation benefits are reducing EBITDA margins across luxury properties even as RevPAR grows, limiting the net profitability improvement that investors can realise from raw ADR and occupancy gains. These factors substantially limit UAE luxury hotel real estate market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "The UAE luxury hotel investment story in 2025 is a study in the compounding advantage of being first. Dubai built its luxury hospitality infrastructure the Burj Al Arab, the Atlantis, the Dubai Mall adjacency cluster before any other Middle Eastern city committed to luxury tourism at scale. That 20-year head start means that Dubai now has the operational culture, the brand relationships, the airport connectivity, and the event calendar that no competing city in the region can replicate within the current decade. Abu Dhabi's 24% RevPAR growth in 2025 is impressive. Ras Al Khaimah's Wynn Resort will be transformative. But Dubai's 165,339 keys of which 55.9% of upcoming supply is luxury-classified represents a depth of investment and operational ecosystem that makes it the UAE's anchor luxury hotel real estate market for the foreseeable future. The constraint for investors is not RevPAR growth. It is the supply delivery schedule between 2027 and 2030 and whether 12,000 new luxury keys can be absorbed without a multi-year RevPAR compression cycle." Troview Intelligence Head of UAE Luxury Hotel Real Estate Research

SEGMENT INSIGHTS

Three Emirates Shaping UAE Luxury Hotel Real Estate

| Total Hotel Keys (2025) | Luxury Segment ADR (H1 2025) | Luxury RevPAR (H1 2025) | H1 2025 Occupancy |

| 165,339 existing + upcoming | AED 1,470 (~USD 400) | AED 1,100 (~USD 300) | 81% citywide; 78-80% luxury |

Dubai is the UAE's dominant luxury hotel real estate market, hosting 165,339 existing and upcoming hotel keys that represent 55.9% of the UAE's total upcoming hotel supply per Knight Frank UAE Hospitality Market Review data. Dubai's luxury hotel segment operates at premium ADR and RevPAR levels that position it among the highest-performing luxury hotel markets globally: average ADRs of approximately AED 1,470 (USD 400) in H1 2025 with RevPAR of approximately AED 1,100 (USD 300) across the luxury segment, compared with citywide ADR of AED 745 (USD 200) during the same period per verified hospitality intelligence analysis. Dubai's hotel inventory reached 152,300 to 158,700 rooms in 2025 across approximately 730 establishments, with five-star and four-star hotels jointly accounting for 64% of total stock per Cavendish Maxwell Dubai hotel market reporting. The Atlantis The Royal, completed at a USD 1.4 billion investment in 2024, demonstrated that Palm Jumeirah ultra-luxury assets can generate peak ADRs above AED 5,000 (USD 1,360) for suites and implemented an operational model that automated 40% of routine tasks while investing in specialist service roles sommelier teams, wellness experts, experience curators that maintain service quality while controlling personnel cost inflation.

Abu Dhabi FASTEST REVPAR GROWTH, +24% YOY, CULTURAL TOURISM SURGE

| RevPAR Growth (YTD Aug 2025) | ADR Growth (YTD Aug 2025) | City Hotel Occupancy | Cultural Visitation Growth |

| 24% year-on-year | 20.2% year-on-year | 82.8% city hotels | 47% increase in 2025 |

Abu Dhabi recorded the strongest RevPAR performance of any UAE emirate in the year to August 2025, with RevPAR growing 24% and ADR increasing 20.2% year-on-year per Knight Frank UAE Hospitality Market Review, driven by major international events, a 47% increase in cultural visitation from Abu Dhabi's museum and heritage attraction investments including the Louvre Abu Dhabi and planned expansions, and a surge in MICE demand from government-hosted international conferences. City hotel occupancy in Abu Dhabi reached 82.8% with resort occupancy at 78.6% in 2025, outperforming Dubai's citywide occupancy rate and confirming the emirate's ability to sustain premium occupancy alongside significant ADR growth simultaneously. Abu Dhabi National Hotels, UAE, operates a portfolio of over 15 hotels including The Ritz-Carlton Abu Dhabi Grand Canal and Kempinski The Boulevard Dubai, and confirmed record hotel revenues and RevPAR performance in 2025 in line with the emirate's broader hospitality sector milestone year per verified reporting. The planned Naseem Al Bahr Resort and Spa development in Abu Dhabi is positioned as a future luxury anchor for the emirate's resort segment.

| RevPAR Growth (YTD Aug 2025) | ADR Growth (YTD Aug 2025) | Total Hotel Keys (Aug 2025) | Key Project Pipeline |

| 10% year-on-year | 6.6% to AED 618 | 11,902 keys | Wynn Resort (planned gaming resort) |

Ras Al Khaimah is the UAE's third luxury hotel investment destination and the fastest-growing emirate by new luxury hotel supply percentage, with RevPAR growing 10% year-on-year in the year to August 2025 and ADR climbing 6.6% to AED 618 per Knight Frank data, reflecting the emirate's ability to attract HNWI leisure travellers through its combination of mountainous natural landscapes, beach resort infrastructure, and lower luxury accommodation costs compared to Dubai. The planned Wynn Resort represents Ras Al Khaimah's most ambitious luxury hospitality project, incorporating a gaming component that is unique within the UAE market and targeting HNWI travellers seeking luxury experiences that combine casino gaming not available elsewhere in the UAE with the established luxury hospitality infrastructure of a destination that has already attracted Anantara Hotels, Rotana Hotels, and Rixos to develop resort assets. Ras Al Khaimah's competitive advantage for luxury hotel investment is its land availability and lower development cost structure relative to Dubai, allowing resort developers to build at a lower cost per key while still capturing premium ADR through brand relationships and natural asset differentiation.